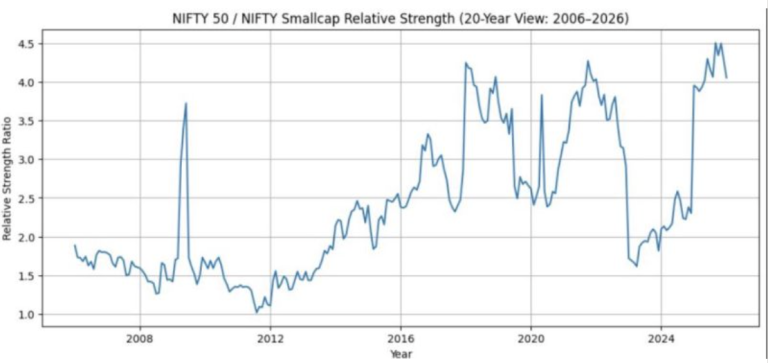

Nifty 50 vs Small Caps, What 20 Years of Market Behaviour Is Telling Us

The graphic above shows the ratio between the Nifty 50 and the Small Cap Index over the last 20 years. This ratio is a simple way to track market leadership. When the ratio falls, small caps outperform large caps, reflecting…