There have been a large number of queries from the retiring officers as regards the commutation of pension and options available for the investment of retirement corpus.

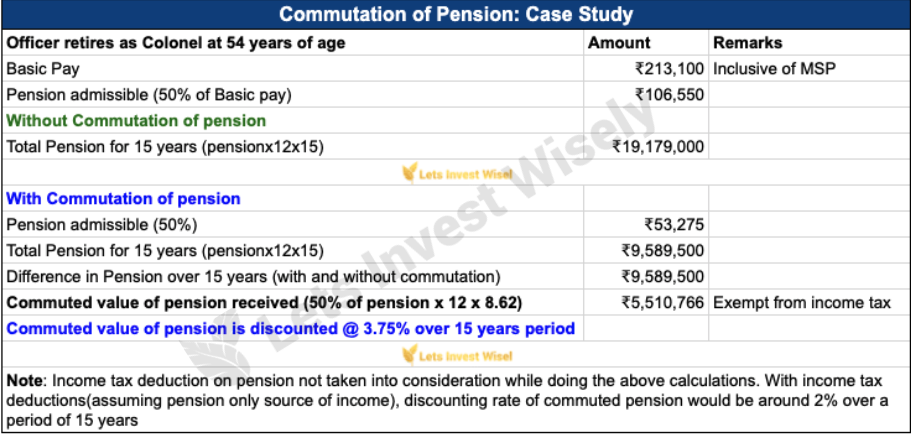

In the Armed Forces, we have the option to commute up to 50% of our pension. This commuted portion is restored after 15 years. The decision to commute or not commute is a personal choice influenced by different factors. However, I strongly believe that every one of us should commute the full 50% of our pension. Now, let’s delve into the calculations behind this decision. To illustrate, let’s consider the case of an officer retiring with a pension amount of 1,06,550/-.

To be beneficial, the commuted value of a pension should aim to earn a little over 3.75% annually. This can be easily achieved by investing the money in a conservative approach like a bank fixed deposit (FD). Additionally, it’s important to consider the future value of the un-commuted portion of the pension by discounting it for inflation over the next 15 years. This depreciation accounts for the impact of inflation on the un-commuted portion

The commuted value of the pension can pay off liabilities, fund children’s education and weddings, or earn higher returns over 15 years. If an officer passes away, the next of kin receives a full pension without deducting the commuted portion for up to seven years.

Investments are based on risk profile, financial goals, and available time. However, many of us believe in parking the money in ‘safe’ assets like small saving schemes in post offices, taxable bonds by RBI, and bank fixed deposits.

Despite offering low returns, no tax benefits, and imposing long lock-in periods, small saving instruments provide a sense of safety even if the real value (adjusted for taxation and inflation) falls below the initial investment. Let’s illustrate this with an example: investing Rs 1.50 crore in various small saving schemes to evaluate the maturity and real value outcomes. Over 5 and 10 years, the real value of the initial investments has declined by 8.66% and 16% respectively.

Let’s explore the outcome of investing Rs 1.50 crore in alternative options such as Equity, Debt, and Hybrid Mutual Fund (MF) schemes. We’ll analyze the maturity amount and real value results. Over 5 and 10 years, the real value of the initial investments has increased by 11.34% and 25.3% respectively. This improved performance can be attributed to tax incentives and a higher return on investments (assuming a 12% RoI for equity mutual funds, aligning with long-term averages of 12-15%).

Highlights: Investment of Retirement Corpus

- In the case of traditional investments, the real value of the initial investments (adjusted for tax and inflation) is negative for both the 5-year and 10-year investment periods. This is mainly attributed to low returns on investment (RoI) and the absence of tax benefits.

- In the case of other investment options, the real value of the initial investments is positive for both the 5-year and 10-year investment periods. This is mainly due to the superior returns on investments (RoI) and the presence of tax benefits, as explained in the second option.

- Net RoI duly adjusted against tax needs to beat the inflation for the positive real value of investments

Conclusion

- “ Mutual Funds are subject to market risk; read all documents carefully before investing” Let this warning not scare us. Yes, there is a market risk but look at the history and growth. The Mutual Fund industry has grown five times over the last 10 years and has around 45 lakh crores (12% of Indian GDP) of assets under management. (Data from AMFI website)

- It’s important to beat inflation for money to grow in real terms. Equity has been the best-performing asset class over the last four decades.

- Choose the mix of the right asset classes based on risk profile and financial goals. Plan the investment of retirement corpus through mutual funds

- Investing through mutual funds offers the convenience of investing across various asset classes, along with lower fees and better performance. It allows investors to retain control over their investments, making it a favorable option.

- Please don’t be shy about taking professional advice if we do not understand the intricacies of the investments.

Need to talk more about this or any other issue related to personal finance? Please feel free to call or book a no-charge consultation with me on this link. (https://calendly.com/rakeshgoyal). Confidentiality is assured.

As you are aware, I send out a regular email with an in-depth analysis of relevant topics around personal finance. If your friends, coursemates, or relatives wish to join the mailing list (with over 4400+ people already subscribed), they can signup here

To remain updated on money matters, join our telegram group “Lets Invest Wisely” at https://t.me/+SB3F7hQPbxNlMTc1

Lets Invest Wisely, a leading financial services firm helps you with

- Prioritizing your financial goals with a customised investment plan

- Retirement plan based on your specific requirements

- Tax planning,

- Insurance planning,

- Wealth creation and

- Estate Planning

We help you invest through mutual funds, Portfolio Management Services(PMS), Corporate FDs, and Term Insurance to protect your family from financial loss in case of loss of life and plan distribution of your assets to your next generation through estate planning (Writing of Will, creation of a family trust, etc)

Contact us at 7341137190 or mail us at rakesh@letsinvestwisely.com

#investwisely