| Rates of interest on various small saving schemes have been slashed substantially by the Government of India wef 01 April 2020. The annual rate of interest on Bank Savings Account would be around 2.75% and Bank FDs will fetch you 5.5% to 5.8% for one to three years of term deposit. Further, interest accrued on these investments is fully taxable (except upto Rs 10000 on a savings account). So for example, three years Bank FD having an annual rate of interest in the range of 5.8% will effectively generate a 4.06% return on investment (RoI) post taxation assuming a 30% tax bracket. With annual inflation hovering around 5% we are actually losing out on the purchasing value of our money by keeping it in Bank FD. So, is there any option available better than keeping money in a bank fixed deposit or savings account? Yes, investing money in debt mutual funds offer the following benefits: * Better returns on investments (7 – 8%) * Less tax liability, no tax deducted at source (TDS) * Qualify for long term capital gains if remain invested for three years or more (20% tax rate with indexation benefits) * Liquidity as good as bank account |

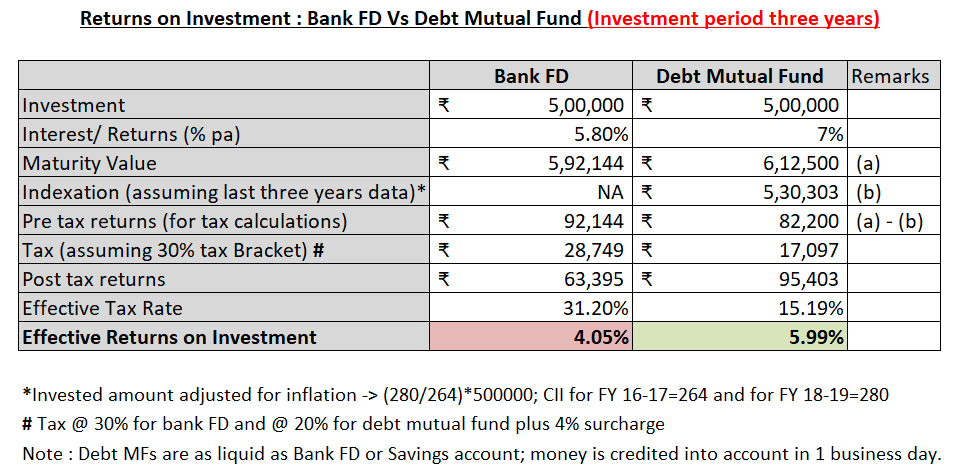

Let’s understand this with the help of an example. For calculation purposes, let’s assume we invested Rs 5 lakh for 3 years in bank fixed deposit (RoI 5.8%) as well as in debt fund (RoI 7%).

So in the above example, we have seen that effective tax rate in debt mutual fund is half to that of bank fixed deposit and return on investment is 50% more than bank FD.

Happy Investing!!

Disclaimer: Mutual funds are subject to market risk. Read all related documents carefully before investing.

#investwisely