Nifty 50 vs Small Caps, What 20 Years of Market Behaviour Is Telling Us

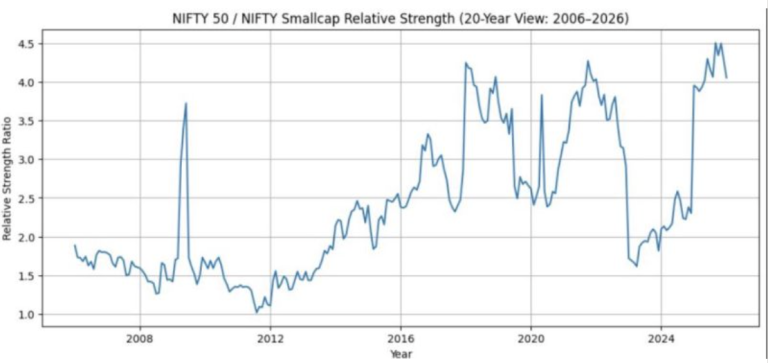

The graphic above shows the ratio between the Nifty 50…

The graphic above shows the ratio between the Nifty 50…

We are living in the loudest investing environment in history.…

This single mother investing guide is designed for those carrying…

Direct mutual funds are cheaperSo why would anyone choose Regular…

Every time the Rupee weakens against the US Dollar, a…

Open any social media platform today, and you’re flooded with…

“Now, your investments don’t have to wait for the market…

We all talk about compounding, how small amounts grow big…

“Investing is simple; it’s our behaviour as humans that makes…